FMN Plc Investment Pitch – GA Academy 3.0

This stock pitch was prepared by Basirat Adebiyi, Abbas Bashar, Oluwatobi Sholanke, and Chigbo Oguejiofor as part of their project during the recently concluded Gifted Analysts Academy 3.0

Research and Analytics

Research and Analytics

This stock pitch was prepared by Basirat Adebiyi, Abbas Bashar, Oluwatobi Sholanke, and Chigbo Oguejiofor as part of their project during the recently concluded Gifted Analysts Academy 3.0

Currently, the local drugs manufacturers are faced with an intense competition from imported products and multinational companies. For instance, 70% of the drugs consumed in Nigeria are imported. Also, almost all the local manufacturers source their active pharmaceuticals ingredients or raw material through importation. The preceding suggests that they are merely purchasing drugs and repackaging them for use. These account for the major challenge in the pharmaceutical industry in Nigeria. Though, Fidson is currently working to expand into Active pharmaceutical production (API). Other constraints, will be infrastructural challenges such as inconsistent energy, weak technology, scarcity of forex and high taxation etc.

Dangote Sugar Refinery PLC (DANGSUGAR) recently released its H1-22 financial performance, showing top line and bottom line growth of 40.5% y/y and 60.6% y/y, respectively. In this report, one of our trainees at the GA Academy 2.0 analysed the company’s financial performance and update our outlook for the rest of the year.

We arrived at a target price of N24.6 per share on Transcorp hotel PLC based on a mix of two valuations metrics- the DCF model with an intrinsic share value of N27, and the DDM with an intrinsic share value of N22. We attributed a weight of 60% and 40% to each methodology, respectively, to arrive at our target price.

The existing revenue-sharing structure of the government stifles innovation and prevents the state from looking inward to improve revenue since the Federal Allocation remains intact. The major source of revenue for most States is the funding from FAAC, with many contributing little to the pool. Oil revenues which make up more than 42% of government income are generated from activities in oil-producing states, mainly in the South-South region, a fraction of the nation.

Imagine you’re a policymaker in sub-Saharan Africa. You’ve been charged with lifting your country out of the worst health crisis in living memory, and nobody around you knows when it will end—the second wave that gripped the region earlier in the year has eased, but many countries are nonetheless bracing for further waves as winter approaches.

One piece of good news is that a global recovery is well underway. Key economies are rebounding sharply, global trade has improved, commodity prices are higher, and investment flows have resumed.

The bad news is that, for sub-Saharan Africa, at least, near-term growth prospects are somewhat more subdued. And as long as widespread vaccination remains out of reach, you will face the unenviable task of trying to boost your economy while simultaneously dealing with repeated COVID-19 outbreaks as they arise.

Although revenue declined, we note that the cost of sales surged during the period. Specifically, cost of sales was N103.94 billion compared to N70.65 billion recorded in the corresponding period of 2019. This was due to 95% increase in operational and maintenance expenses (N23.56 billion) and 59.4% increase in depletion, depreciation and amortisation (N33.75 billion).

Gross profit grew by 13.6% compared to the corresponding period of 2019. The gross profit growth is however slow due to the fact that the growth in cost of sales was more than the growth in revenue. While revenue grew by 13.6% y/y, the cost of sales grew by 28.8%. Hence, gross profit printed N71.73 billion.

In the first 9 months of 2020, Dangote Cement (DANGCEM) plc was able to grow its revenue by 12% on the basis of solid production volume (+5.6% y/y to 18.40 million tonnes) with an overall effect on sales volume (+6.6% y/y to 19.21 million tonnes).

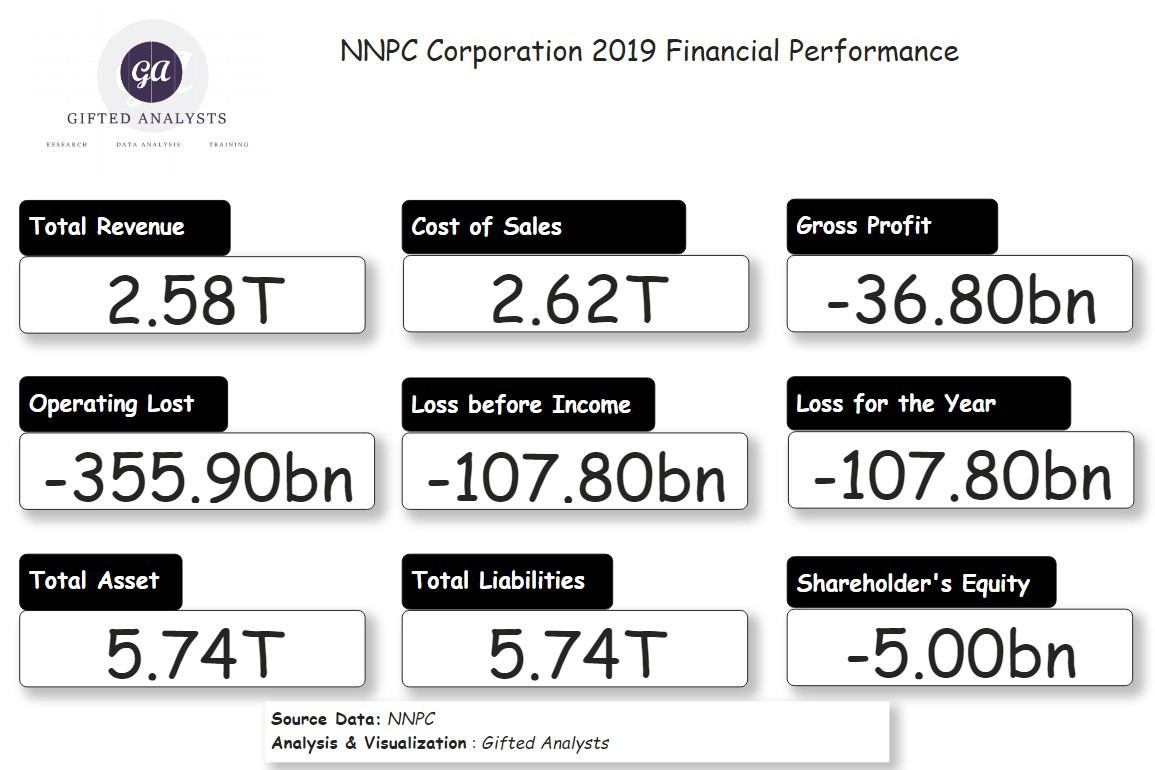

A simple analysis of the 2019 NNPC Group and NNPC Corporation Financial Performance