FMN Plc Investment Pitch – GA Academy 3.0

This stock pitch was prepared by Basirat Adebiyi, Abbas Bashar, Oluwatobi Sholanke, and Chigbo Oguejiofor as part of their project during the recently concluded Gifted Analysts Academy 3.0

Research and Analytics

Research and Analytics

This stock pitch was prepared by Basirat Adebiyi, Abbas Bashar, Oluwatobi Sholanke, and Chigbo Oguejiofor as part of their project during the recently concluded Gifted Analysts Academy 3.0

We issue a sell recommendation on BUA Cement PLC(BUACEMENT.NSE) Based on a target price of ₦58.6k representing a 13% downside on the closing price of ₦70.75 as of march 30th, 2022. Our valuation is based on a methodology mix of Discounted cash flow model (70%), Dividend discount model (10%) and Multiples valuation (20%).

Flour Mill of Nigeria Plc is one of the leading FMCG and a top market player in the flour-based product market. It is the first company to have constructed Nigeria’s first

wheat mill plant. With 60 years of success celebration, the firm has been able to diversify its core business of food through backward integration into other three revenue-generating segments which include Agro-allied, Sugar, and support services. Growth in these three classes of revenue has been impressive at a CAGR of 23.58%

over the past five years. These three segments reported total revenue of N293 billion (or 38.01% of total revenue) in FY-2021 compared to the N102 billion (or 19.4% of

total revenue) in FY-2017. The firm’s ability to expand its portfolio size with an explosive growth of this 23.58% CAGR validates its capacity to provide long-term value creation to shareholders while pursuing a de-risk business opportunity.

2020 was a year of extremes. Travel all but ceased for a period. Oil prices wildly fluctuated. Trade in medical products reached new heights. Household spending shifted to consumer goods rather than services and savings ballooned as people stayed home amid a global shutdown.

In our latest External Sector Report we found that the global reaction to the pandemic further widened global current account balances—the sum of absolute deficits and surpluses among all countries—from 2.8 percent of world GDP in 2019 to 3.2 percent of GDP in 2020. Those balances are set to widen further as the pandemic continues to rage in much of the world.

The growth of infections in sub-Saharan Africa is now the fastest in the world, with an explosive trajectory that is outpacing the record set in the second wave. At this pace, this new wave will likely surpass previous peaks in a matter of days—and in some countries, infections are already more than double, or even triple, their January peaks. The latest (delta) variant—reportedly 60 percent more transmissible than earlier variants—has been detected in 14 countries.

Imagine you’re a policymaker in sub-Saharan Africa. You’ve been charged with lifting your country out of the worst health crisis in living memory, and nobody around you knows when it will end—the second wave that gripped the region earlier in the year has eased, but many countries are nonetheless bracing for further waves as winter approaches.

One piece of good news is that a global recovery is well underway. Key economies are rebounding sharply, global trade has improved, commodity prices are higher, and investment flows have resumed.

The bad news is that, for sub-Saharan Africa, at least, near-term growth prospects are somewhat more subdued. And as long as widespread vaccination remains out of reach, you will face the unenviable task of trying to boost your economy while simultaneously dealing with repeated COVID-19 outbreaks as they arise.

While it’s had some ups and downs, the stock market has soared to historic heights in recent years. For many, that’s great news: it’s a sign that the economy and their retirement accounts are doing really well. For Jan Eeckhout, however, the booming stock market is a sign that there’s something deeply wrong with the economy.

Sure, the economist says, he has a retirement account with stocks, and he personally benefits from the ongoing bonanza on stock exchanges. But the rocket ride of the stock market is powered by the exploding profits of increasingly powerful corporations. Their increasingly ridiculous profits, he says, are eating the income of the vast bulk of workers and hurting the overall economy. That notion is the central thesis of his forthcoming book, The Profit Paradox: How Thriving Firms Threaten the Future of Work.

The rise in long-term US interest rates has become a focus of global macro-financial concerns. The nominal yield on the benchmark 10-year Treasury has increased about 70 basis points since the beginning of the year. This reflects in part an improving US economic outlook amid strong fiscal support and the accelerating recovery from the COVID-19 crisis. So an increase would be expected. But other factors like investors’ concerns about the fiscal position and uncertainty about the economic and policy outlook may also be playing a role and help explain the rapid increase early in the year.

Each time the word housing pops up, especially the challenges that come with owning /acquiring a house, Affordable Housing or Housing Affordability follows as it is one of the major, if not the most severally cited, housing problems in the whole wide world. With a housing gap of 17 to 20 million units and a low estimated homeownership rate of 25%, Nigeria is not left behind in this problem. According to a UN report, Nigeria’s population is about 186 million. Over 60% of these people will be living in urban areas in the coming years, hence needing a long-term plan to make housing accessible and affordable in the country. There are too many obstacles and bottlenecks in the housing sector, including the land use act. In this article, I highlight ways housing can be more accessible irrespective of the sector’s challenges.

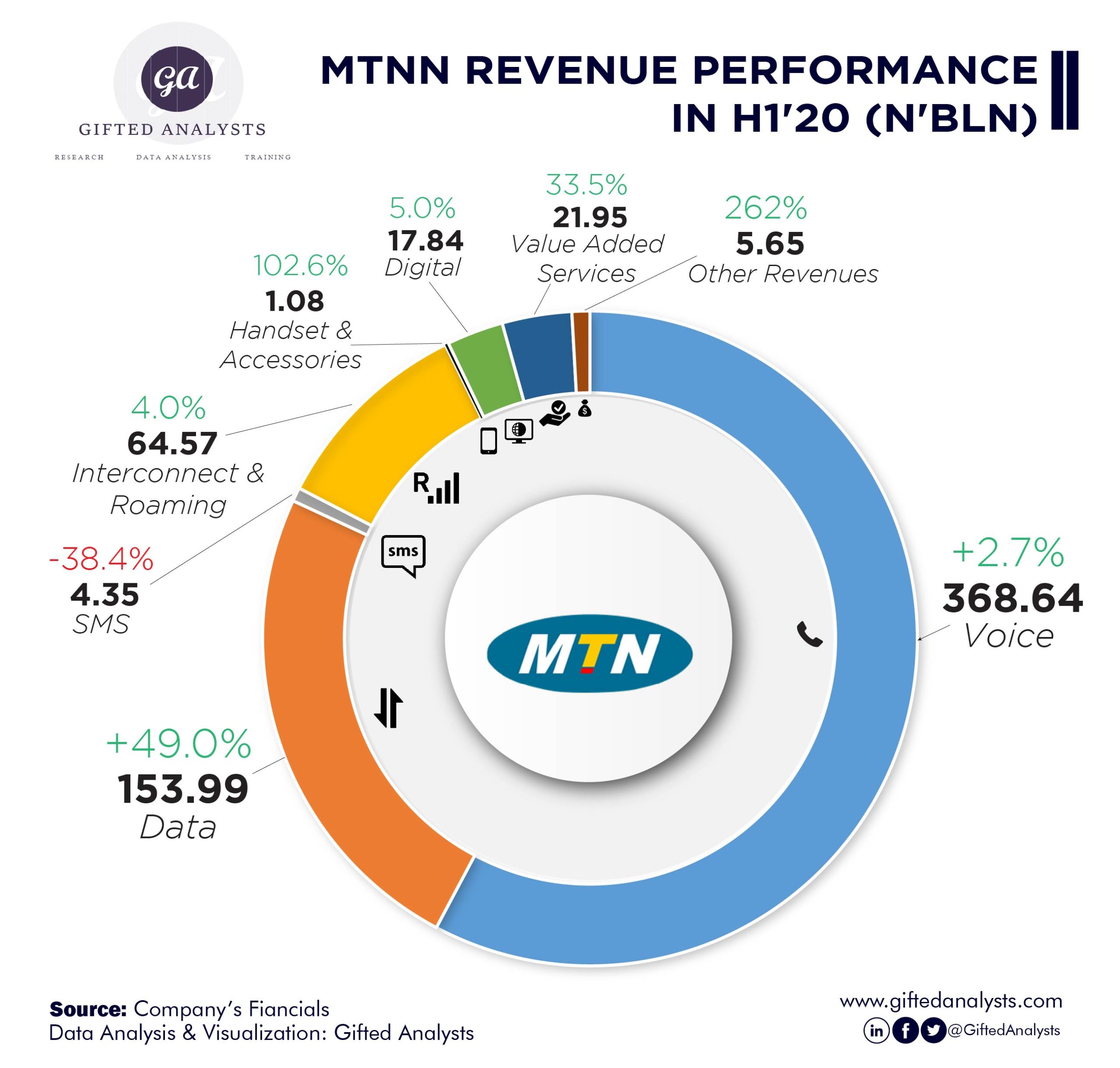

MTN Nigeria increased its subscribers base by adding 6.8m to its network totaling 71.1m mobile subscribers as of June 2020. Total revenue generated was up by 12.5% (y/y) to ₦638.08bn for the first half of the year, compared to ₦566.95bn generated in the same period in 2019. Growth in revenue was largely driven by a 12.6% increase in revenue from Services provided which accounted for 99.8% of total revenue (₦636.99bn).

Service revenue included revenue from its core activities of providing voice calls, data services, digital platforms, fintech (MoMo), and Other services (SMS, USSD, etc.).