By Gita Gopinath / IMF

The COVID-19 pandemic continues to spread with over 1 million lives tragically lost so far. Living with the novel coronavirus has been a challenge like no other, but the world is adapting. As a result of eased lockdowns and the rapid deployment of policy support at an unprecedented scale by central banks and governments around the world, the global economy is coming back from the depths of its collapse in the first half of this year. Employment has partially rebounded after having plummeted during the peak of the crisis.

This crisis is however far from over. Employment remains well below pre-pandemic levels and the labor market has become more polarized with low-income workers, youth, and women being harder hit. The poor are getting poorer with close to 90 million people expected to fall into extreme deprivation this year. The ascent out of this calamity is likely to be long, uneven, and highly uncertain. It is essential that fiscal and monetary policy support are not prematurely withdrawn, as best possible.

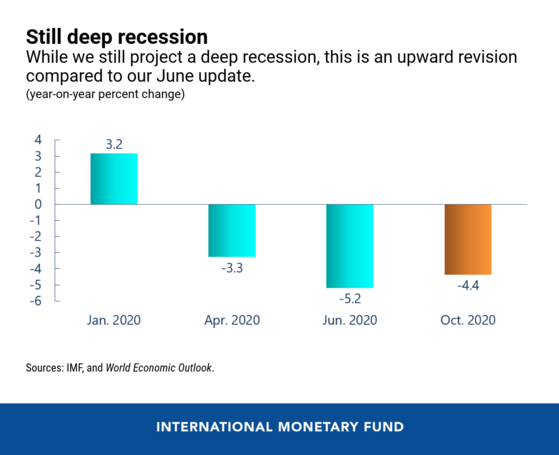

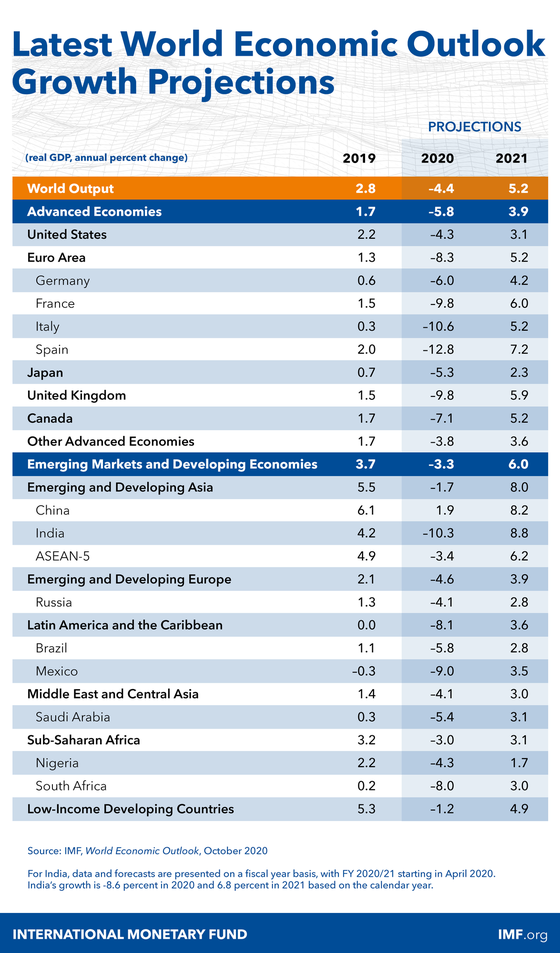

In our latest World Economic Outlook, we continue to project a deep recession in 2020. Global growth is projected to be -4.4 percent, an upward revision of 0.8 percentage points compared to our June update. This upgrade owes to somewhat less dire outcomes in the second quarter, as well as signs of a stronger recovery in the third quarter, offset partly by downgrades in some emerging and developing economies. In 2021 growth is projected to rebound to 5.2 percent, -0.2 percentage points below our June projection.

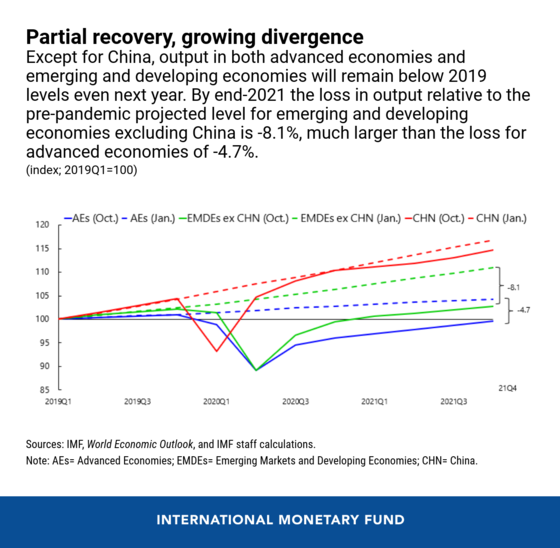

Except for China, where output is expected to exceed 2019 levels this year, output in both advanced economies and emerging market and developing economies is projected to remain below 2019 levels even next year. Countries that rely more on contact-intensive services and oil exporters face weaker recoveries compared to manufacturing-led economies.

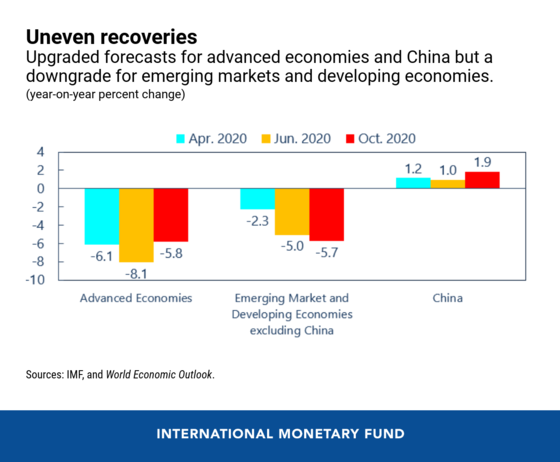

The divergence in income prospects between advanced economies and emerging and developing economies (excluding China) triggered by this pandemic is projected to worsen. We are upgrading our forecast for advanced economies for 2020 to -5.8 percent, followed by a rebound in growth to 3.9 percent in 2021. For emerging market and developing countries (excluding China) we have a downgrade with growth projected to be – 5.7 percent in 2020 and then a recovery to 5 percent in 2021. With this, the cumulative growth in per capita income for emerging-market and developing economies (excluding China) over 2020-21 is projected to be lower than that for advanced economies.

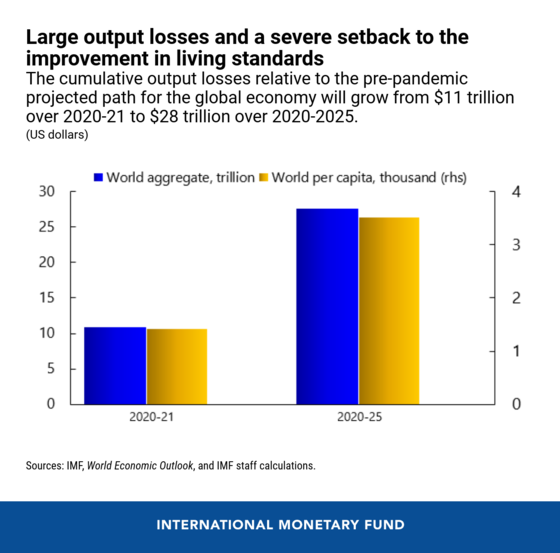

This crisis will likely leave scars well into the medium term as labor markets take time to heal, investment is held back by uncertainty and balance sheet problems, and lost schooling impairs human capital. After the rebound in 2021, global growth is expected to gradually slow to about 3.5 percent into the medium term. The cumulative loss in output relative to the pre-pandemic projected path is projected to grow from 11 trillion over 2020-21 to 28 trillion over 2020-25. This represents a severe setback to the improvement in average living standards across all country groups.

There remains tremendous uncertainty around the outlook with both downside and upside risks. The virus is resurging with localized lockdowns being re-instituted. If this worsens and prospects for treatments and vaccines deteriorate, the toll on economic activity would be severe, and likely amplified by severe financial market turmoil. Growing restrictions on trade and investment and rising geopolitical uncertainty could harm the recovery. On the upside, faster and more widespread availability of tests, treatments, vaccines, and additional policy stimulus can significantly improve outcomes.

More Action is Needed

The considerable global fiscal support of close to $12 trillion and the extensive rate cuts, liquidity injections, and asset purchases by central banks helped saved lives and livelihoods and prevented a financial catastrophe.

There is still much that needs to be done to ensure a sustained recovery. First, greater international collaboration is needed to end this health crisis. Tremendous progress is being made in developing tests, treatments and vaccines, but only if countries work closely together will there be enough production and widespread distribution to all parts of the world. We estimate that if medical solutions can be made available faster and more widely relative to our baseline, it could lead to a cumulative increase in global income of almost $9 trillion by end 2025, raising incomes in all countries and reducing income divergence.

Second, to the extent possible, policies must aggressively focus on limiting persistent economic damage from this crisis. Governments should continue to provide income support through well targeted cash transfers, wage subsidies, and unemployment insurance. To prevent large scale bankruptcies and ensure workers can return to productive jobs, vulnerable but viable firms should continue to receive support—wherever possible—through tax deferrals, moratoria on debt service, and equity-like injections.

Over time, as the recovery strengthens, policies should shift to facilitating reallocation of workers from sectors likely to shrink on a long-term basis (travel) to growing sectors (e-commerce). Workers should be supported through this adjustment with income transfers, retraining, and reskilling. Supporting reallocation will also require steps to speed up bankruptcy procedures and resolution mechanisms to efficiently tackle firm insolvencies. A public green infrastructure investment push in times of low interest rates and high uncertainty can significantly increase jobs and accelerate the recovery, while also serving as an initial big step towards reducing carbon emissions.

Emerging market and developing economies are having to manage this crisis with fewer resources, as many are constrained by elevated debt and higher borrowing costs. These economies will need to prioritize critical spending for health and transfers to the poor and ensure maximum efficiency. They will also need continued support in the form of international grants and concessional financing, and debt relief in some cases. Where debt is unsustainable it should be restructured sooner than later to free up finances to deal with this crisis.

Lastly, policies should be designed with an eye toward placing economies on paths of stronger, equitable, and sustainable growth. The global easing of monetary policy while essential for the recovery should be complemented with measures to prevent build-up of financial risks over the medium term, and central bank independence should be safeguarded at all costs. Needed fiscal spending and the output collapse have driven global sovereign debt levels to a record 100 percent of global GDP. While low interest rates alongside the projected rebound in growth in 2021 will stabilize debt levels in many countries, all will benefit from a medium-term fiscal framework to give confidence that debt remains sustainable. In the future, governments will likely need to raise the progressivity of their taxes while ensuring that corporations pay their fair share of taxes, alongside eliminating wasteful spending.

Investments in health, digital infrastructure, green infrastructure and education can help achieve productive, inclusive, and sustainable growth. And expanding the safety net where gaps exist can ensure the most vulnerable are protected while supporting near-term activity.

This is the worst crisis since the Great Depression, and it will take significant innovation on the policy front, at both the national and international levels to recover from this calamity. The challenges are daunting. But there are reasons to be hopeful. The exceptional policy response, including the establishment of the European Union pandemic recovery package fund and the use of digital technologies to deliver social assistance are a powerful reminder that well-designed policies protect people and collective economic wellbeing. At the IMF we have provided funding at record speed to 81 members since the start of the pandemic, granted debt relief, and called for extended debt service suspension for low-income countries and for reform of the international debt architecture. Building on these actions, policies for the next stage of the crisis must seek lasting improvements in the global economy that create prosperous futures for all.

Credit: The Post A long, Uneven and Uncertain Ascent first appeared in the IMF Blog on 13th October 2020.