By Sonali Das and Philippe Wingender / IMF

Recessions wreak havoc and the damage is often long-lived. Businesses shut down, investment spending is cut, and people out of work can lose skills and motivation as the months stretch on. But the recession brought on by the COVID-19 pandemic is no ordinary recession. Compared to previous global crises, the contraction was sudden and deep—using quarterly data, global output declined about three times as much as in the global financial crisis, in half the time.

Systemic financial stress—associated with long-lasting economic damage—has been largely avoided so far, owing to the unprecedented policy actions taken. However, the path to recovery remains challenging, especially for countries with limited fiscal space, and is made harder by the differential impact of the pandemic.

Lessons from history

The extent of the recovery will depend on the persistence of the economic damage, or “scarring,” in the medium-term. This will vary across countries, depending on the future path of the pandemic; the share of high-contact sectors; the ability of businesses and workers to adapt; and the effectiveness of policy responses.

These unknowns make it hard to predict the extent of scarring but there are some lessons we can draw from history. Severe recessions in the past, particularly deep ones, have been associated with persistent output losses from reduced productivity. Although the pandemic has spurred increased digitalization and innovation in production and delivery processes—at least in some countries—the resource reallocation needed to adapt to a new normal may be larger than in past recessions, affecting productivity growth going forward. Another risk is the pandemic-driven rise in market power of dominant firms, which are becoming increasingly entrenched as competitors collapse.

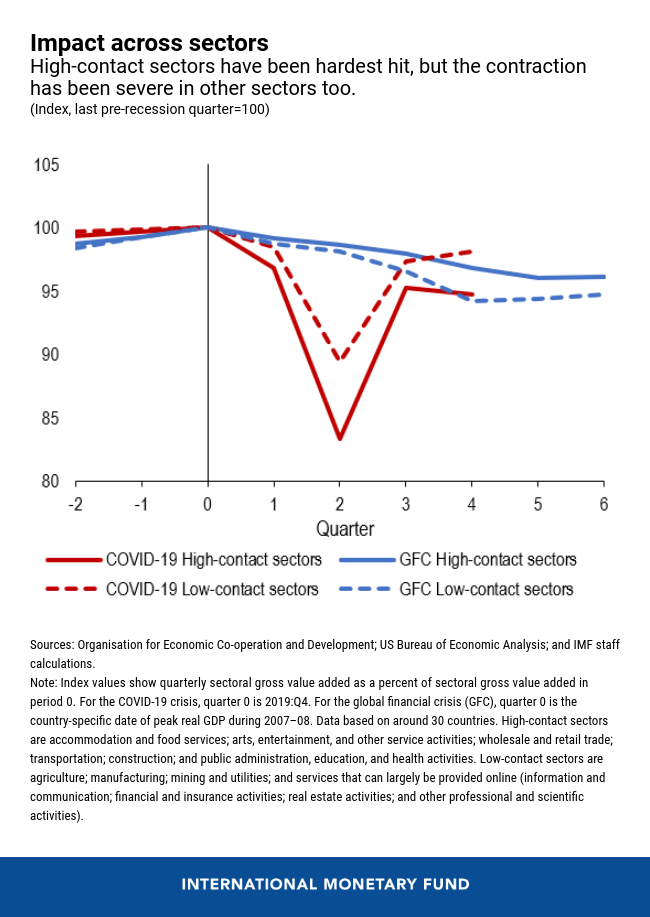

Productivity has also been affected by COVID-19 disruptions to production networks. High-contact sectors, such as arts and entertainment, accommodation and restaurants, and wholesale and retail trade are less central to production networks than, say, the energy sector. But historical analysis shows that even shocks to these peripheral sectors can be greatly amplified through spillovers to other sectors. The closure of restaurants and bars, for example, can affect farms and wineries, resulting in lower demand for tractors and other agricultural equipment. So, although the pandemic’s initial impact was concentrated in higher-contact service sectors, given the size of the disruption, it still resulted in a broad downturn.

Medium-term implications

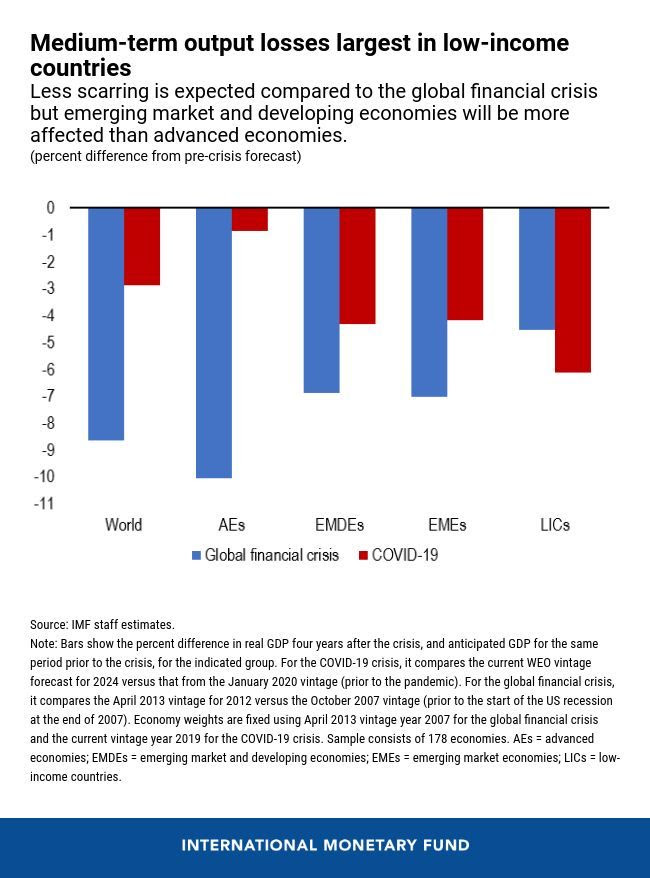

Despite higher-than-anticipated growth as the global economy recovers from the COVID-19 shock, we expect world output in the medium-term to be about 3 percent lower in 2024 than pre-pandemic projections. Because financial stability has largely been preserved, this expected scarring is less than what we saw following the global financial crisis.

However, unlike what happened during the global financial crisis, emerging market and developing economies are expected to have deeper scars than advanced economies, with losses expected to be largest among low-income countries.

This divergence across countries is the consequence of varying economic structures and the size of countries’ fiscal policy responses. Because of how the virus is transmitted, economies that are more reliant on tourism or have a larger share of high-contact sectors, such as the Pacific Islands and the Caribbean, are projected to experience more persistent losses. GDP in the Pacific Islands, for example, is estimated to be 10 percent lower in 2024 than pre-pandemic projections. Many of these countries also have more limited policy space and capacity to mount major health responses or support livelihoods.

Widespread school closures have occurred across countries, but the adverse impacts on learning and skills acquisition have been larger in low-income countries. The resulting long-term individual earnings losses and damages to aggregate productivity could be a key legacy of the COVID-19 crisis.

Policies to limit scarring

Experience from past recessions underscores the importance of avoiding financial distress and ensuring effective policy support until the recovery is firmly underway.

Countries will need to tailor their policies to the different stages of the pandemic with a combination of better-targeted support for affected households and firms, and public investments. As vaccine coverage improves and supply constraints ease, these efforts should focus on three priorities:

- First, reversing the setback to human capital accumulation. To address the rise in inequality that is likely to result from the pandemic, social safety nets should be expanded, and adequate resources allocated to healthcare and education.

- Second, supporting productivity through policies to facilitate job mobility and promote competition and innovation.

- Third, boosting public infrastructure investment, particularly in green infrastructure to help crowd-in private investment.

Finally, strong international cooperation will be needed to address the growing divergence across countries. It is vital that financially constrained economies have adequate access to international liquidity for development spending. On the health front, this also means ensuring adequate production and universal distribution of vaccines—including through sufficient funding for the COVAX facility—to help developing countries beat back the pandemic and prevent even worse scarring.

Sonali Das is a senior economist in the World Economic Studies Division in the IMF’s Research Department.

Philippe Wingender is an economist in the Tax Policy Division of the Fiscal Affairs Department at the IMF.

Credit: The Post Slow-Healing Scars: The Pandemic’s Legacy first appeared in the IMF Blog on 31st March 2021.