By Martin Kaufman and Daniel Leigh / IMF

The world entered the COVID-19 pandemic with persistent, pre-existing external imbalances. The crisis has caused a sharp reduction in trade and significant movements in exchange rates but limited reduction in global current account deficits and surpluses. The outlook remains highly uncertain as the risks of new waves of contagion, capital flow reversals, and a further decline in global trade still loom large on the horizon.

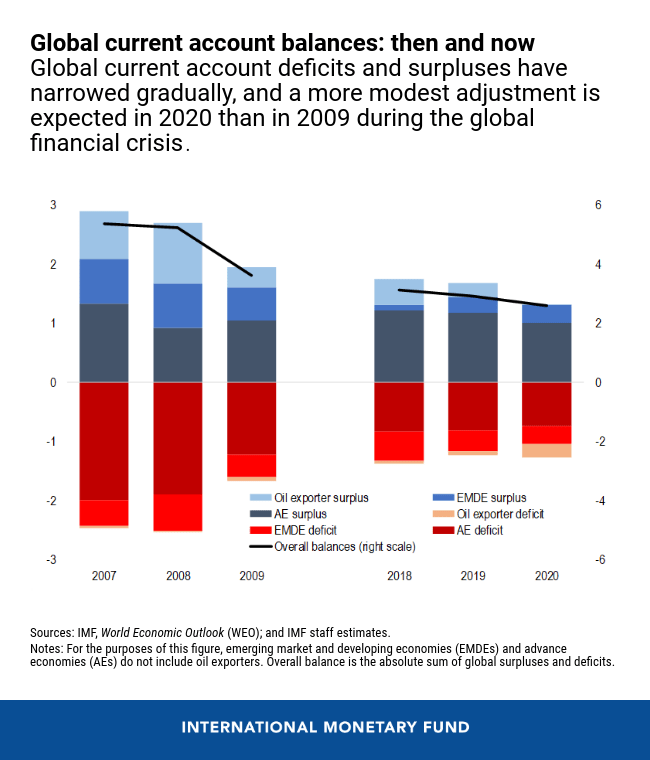

Our new External Sector Report shows that overall current account deficits and surpluses in 2019 were just below 3 percent of world GDP, slightly less than a year earlier. Our latest forecasts for 2020 imply only a further narrowing by some 0.3 percent of world GDP, a more modest decline than after the global financial crisis 10 years ago.

The immediate policy priorities are to provide critical relief and promote economic recovery. Once the pandemic abates, reducing the world’s external imbalances will require collective reform efforts by both excess surplus and deficit countries. New trade barriers will not be effective in reducing imbalances.

Why imbalances matter

External deficits and surpluses are not necessarily a cause for concern. There are good reasons for countries to run them at certain points in time. But economies that borrow too much and too quickly from abroad, by running external deficits, may become vulnerable to sudden stops in capital flows. Countries also face risks from investing too much of their savings abroad given investment needs at home. The challenge lies in determining when imbalances are excessive or pose a risk. Our approach focuses on each country’s overall current account balance and not its bilateral trade balances with various trading partners, as the latter mainly reflect the international division of labor rather than macroeconomic factors.

We estimate that about 40 percent of global current account deficits and surpluses were excessive in 2019 and, as in recent years, concentrated in advanced economies. Larger-than-warranted current account balances were mostly in the euro area (driven by Germany and the Netherlands) with lower-than-warranted current account balances mainly existing among Canada, the United Kingdom, and the United States. China’s assessed external position remained, as in 2018, broadly in line with fundamentals and desirable policies, due to offsetting policy gaps and structural distortions.

Our report offers individual economy assessments of external imbalances and exchange rates for the 30 largest economies. Over time, these imbalances have accumulated, with the stocks of external assets and liabilities now at historic highs, potentially raising risks for both debtor and creditor countries. The persistence of global imbalances and mounting perceptions of an uneven playing field for trade has fueled protectionist sentiments, leading to a rise in trade tensions between the US and China. Overall, many countries had pre-existing vulnerabilities and remaining policy distortions heading into the crisis.

COVID-19: An intense external shock

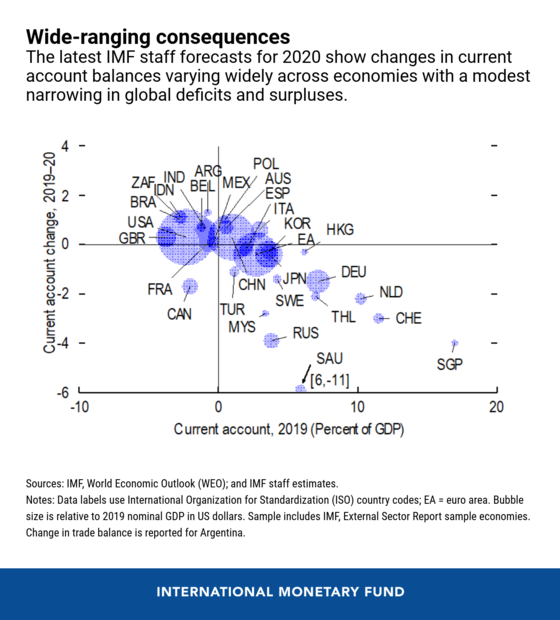

With the world economy still grappling with the COVID-19 crisis, the external outlook is highly uncertain. Even though we forecast a slight narrowing of global imbalances in 2020, the situation varies around the world. Economies dependent on severely affected sectors, such as oil and tourism, or reliant on remittances, could see a fall in their current account balances exceeding 2 percent of GDP. Such intense external shocks may have lasting effects and require significant economic adjustments. At the global level, our forecasts imply a more limited narrowing in current account balances than after the global financial crisis a decade ago, which partly reflects the smaller, precrisis global imbalances this time than during the housing and asset price booms of the mid-2000s.

Early in the COVID-19 crisis, tighter external financing conditions triggered sudden capital outflows with sharp currency depreciations across numerous emerging market and developing economies. The exceptionally strong fiscal and monetary policy responses, especially in advanced economies, have promoted a recovery in global investor sentiment since then, with some unwind of the initial sharp currency movements. But many risks remain, including new waves of contagion, economic scarring, and renewed trade tensions.

Another bout of global financial stress could trigger more capital flow reversals, currency pressures, and further raise the risk of an external crisis for economies with preexisting vulnerabilities, such as large current account deficits, a high share of foreign currency debt, and limited international reserves, as highlighted in this year’s analytical chapter. A worsening of the COVID-19 pandemic could also dislocate global trade and supply chains, reduce investment, and hinder the global economic recovery.

Providing relief and rebalancing the world economy

Policy efforts in the near term should continue to focus on providing lifelines and promoting economic recovery. Countries with flexible exchange rates would benefit from continuing to allow them to adjust in response to external conditions, where feasible. Foreign exchange intervention, where needed and where reserves are adequate, could help alleviate disorderly market conditions. For economies facing disruptive balance of payments pressures and without access to private external financing, official financing and swap lines can help provide economic relief and preserve critical health care spending.

Tariff and nontariff barriers to trade should be avoided, especially on medical equipment and supplies, and recent new restrictions on trade rolled back. Using tariffs to target bilateral trade balances is costly for trade and growth, and tends to trigger offsetting currency movements. Tariffs are also generally ineffective for reducing excess external imbalances and currency misalignments, which requires addressing underlying macroeconomic and structural distortions. Modernizing the multilateral rules-based trading system and strengthening rules on subsidies and technology transfer is warranted, including by expanding the rule book on services and e-commerce and ensuring a well-functioning WTO dispute settlement system.

Over the medium term, reducing excess imbalances in the global economy will require joint efforts on the part of both excess surplus and excess deficit countries. Economic and policy distortions that predated the COVID-19 crisis might persist or worsen, suggesting the need for reforms tailored to country-specific circumstances.

In economies where excess current account deficits before the crisis reflected larger-than-desirable fiscal deficits (as in the United States) and where such imbalances persist, fiscal consolidation over the medium term would promote debt sustainability, reduce the excess current account gap, and facilitate raising international reserves where needed (as in Argentina). Countries with export competitiveness challenges would benefit from productivity-raising reforms.

In economies where excess current account surpluses that existed before the crisis persist, prioritizing reforms that encourage investment and discourage excessive private saving are warranted. In economies with remaining fiscal space, a growth-oriented fiscal policy would strengthen economic resilience and narrow the excess current account surplus. In some cases, reforms to discourage excessive precautionary saving may also be warranted (as in Thailand and Malaysia) including by expanding the social safety net.

CREDIT: The Post Global Imbalances and the COVID-19 Crisis first appeared on the IMF Blog on 4th August, 2020