By Martin Mühleisen, Tryggvi Gudmundsson, and Helene Poirson Ward / IMF

The economic impact of the COVID-19 pandemic on emerging market economies far exceeded that of the global financial crisis. Unlike previous crises, the response has been decisive just like in advanced economies. Yet, conventional policies are reaching their limit and unorthodox policies are not without risks.

A pandemic still unfolding

COVID-19 is still to play out fully in the emerging market universe (see chart for country list), posing risks to both people and economies. While countries such as China, Uruguay, and Vietnam have managed to contain the virus, others such as Brazil, India, and South Africa continue to grapple with a rise in infections.

The economic impact has been even more severe as emerging market economies were buffeted by multiple shocks. Compounding the effects of domestic containment measures has been a decline in external demand. Particularly hit are tourism-dependent countries due to a decline in travel and oil exporters as commodity prices plummeted. With global trade and oil prices projected to drop by more than 10 percent and 40 percent respectively, emerging market economies are likely to face an uphill battle. This is even as capital outflows have stabilized and sovereign spreads retreated compared to the sharply volatile market conditions seen in March.

Not surprisingly, the IMF’s latest June World Economic Outlook Update projects emerging market economies to shrink by 3.2 percent this year—the largest drop for this group on record. By way of comparison, in the global financial crisis, growth for the group took a significant hit but still bottomed out at a positive 2.6 percent in 2009.

A decisive policy response

The crisis would have been worse still without the extraordinary policy support. For sure, decisive policy actions in advanced economies led to a turnaround in market conditions that allowed emerging market economies to resume external financing efforts in April and May, which contributed to record levels of bond issuance so far this year—to the tune of $124 billion as of the end of June. But not all countries have seen improved fortunes. Fuel exporters, frontier countries and those with high debt are experiencing a greater financial shock that pushed up borrowing costs, or even worse, denied them further access to markets.

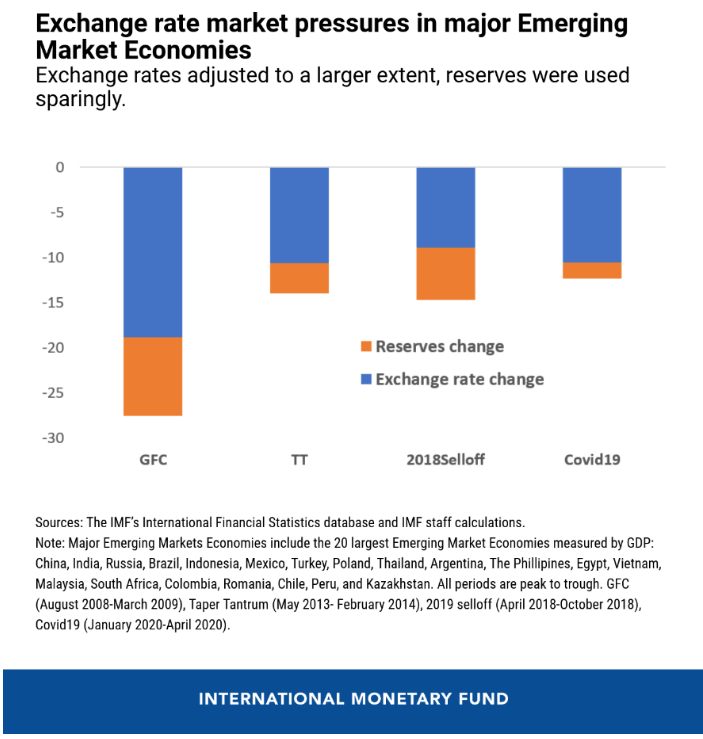

Policy support by advanced economies provided emerging market economy policymakers with wiggle room to soften the economic blow. Unlike previous episodes, where emerging market economies tended to tighten policy to avoid rapid capital outflows and the inflationary effect of exchange rate depreciations, the current crisis has seen emerging market economies’ policy reaction more in line with that of advanced economies (see the IMF’s policy tracker). Most emerging market economies used reserve buffers more sparingly and allowed exchange rates to adjust to a larger extent, while many countries injected liquidity as needed to ensure market functioning. Countries like Poland and Indonesia further eased macroprudential policies to support credit.

Like their more advanced peers, many emerging market economies, including Thailand, Mexico, and South Africa, eased monetary policy during this cycle. In a few cases, limited room to cut policy rates further and distressed market conditions induced use of unconventional monetary policy measures for the first time. These included purchases of government and corporate bonds, although the amounts remain modest so far compared to the larger advanced economies. Conversely, the use of capital flow measures to deter capital outflows has been quite limited so far.

A similar picture is evident on the fiscal policy front. Emerging market economies have relaxed their fiscal stance in an attempt to tackle the health crisis, support people and firms, and offset the economic shocks. While more modest than that of advanced economies, these efforts were significantly greater than during the global financial crisis.

From conventional to unorthodox policies

Despite these actions, the outlook for emerging market economies remains clouded by considerable uncertainty. Chief among many risks is the possibility of a more prolonged health crisis, which would hurt more lives and could have dire economic consequences. Confronting a more severe downturn will be challenging because most emerging markets entered the current crisis with limited room for traditional fiscal, monetary, and external policy support. And much policy room has already been used up by actions undertaken in recent months.

Dwindling policy space may force some countries to take recourse to more unorthodox measures. From price controls and trade restrictions to more unconventional monetary policy and steps to ease credit and financial regulation. Some of these measures—which are also being implemented by some advanced and low-income economies—have significant costs, particularly if used intensively. Export restrictions, for example, could seriously distort the multilateral trading system, and price controls hamper the flow of goods to those who need it most.

The effectiveness of other unorthodox policies will depend on the credibility of the institutions; for instance, whether a country has a track record of credible monetary policy. As we navigate the contours of the ongoing crisis, little time is available to properly analyze the risks and benefits of these actions in a careful manner.

Not out of the woods yet

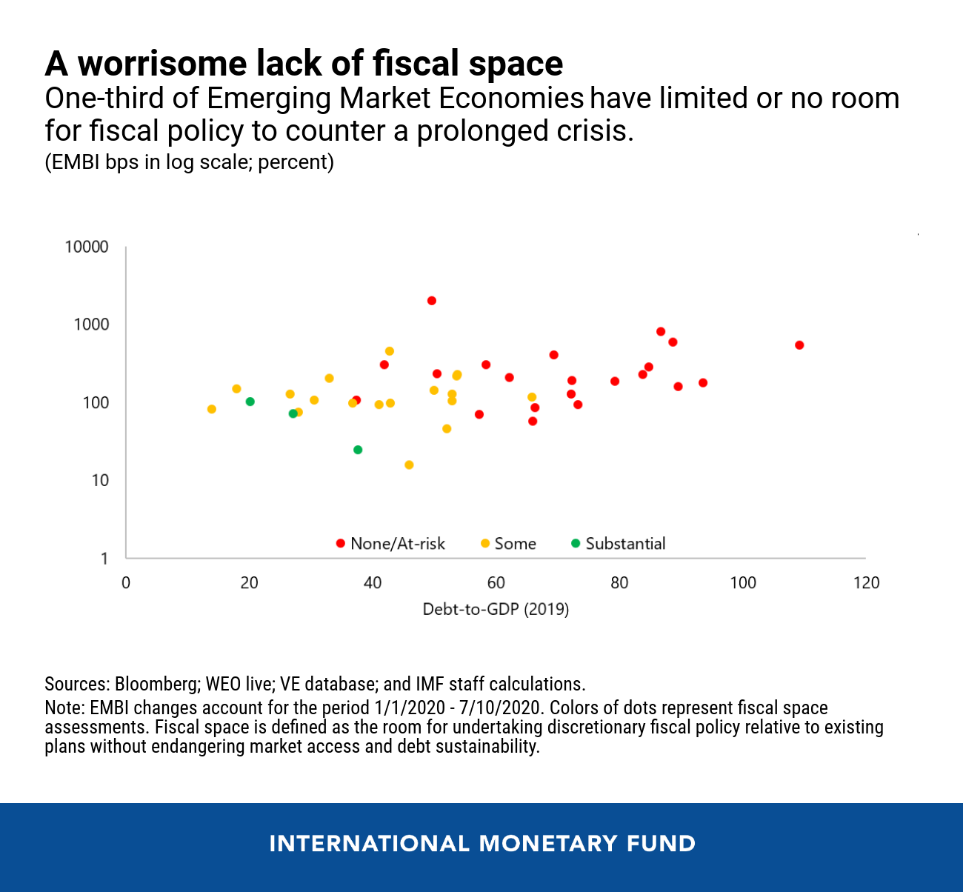

Emerging market economies have navigated the first phase of the crisis relatively well, but the next phase could be much more challenging. The virus remains present, financial conditions are still fragile, and policy space is lower, particularly for those countries facing high risks to debt sustainability. The latter group of countries is quite large. Approximately one third of all emerging market economies entered the crisis with high-debt levels and are assessed to have no space for undertaking additional discretionary fiscal policy, or as having that space significantly at risk.

As the crisis develops, there is also a high risk that liquidity problems morph into solvency concerns. Besides sovereign debt stresses, corporate default risks are alarmingly high in a number of emerging market economies. Moreover, the crisis has hit poor people much harder, and this increase in inequality will amplify policy challenge in many countries.

The complexity of these challenges requires a multi-faceted policy response. First, domestic policies will need to be designed to allow for more durable and inclusive growth. Second, increased support from bilateral and multilateral lenders will be required where market access remains precarious. So far, the IMF has provided 22 emerging market economies with approximately $72 billion (SDR 52 billion) in financial assistance. Finally, for countries where debts prove to be unsustainable, timely and durable resolution of these problems will be needed, by seeking broad burden sharing across creditors including in the private sector. The latter two policy angles will be analyzed in two subsequent blogs on IMF lending and the IMF’s role in debt resolution.

CREDIT: The Post COVID-19 Response in Emerging Market Economies: Conventional Policies and Beyond first appeared in the IMF Blog on 6th August, 2020.