Nigeria is gradually entering another election cycle, and with it comes a familiar question for investors: how do elections affect inflation and equity market performance? Conventional wisdom often assumes that election periods lead to higher inflation and weaker equity markets due to fiscal spending and heightened uncertainty. However, Nigeria’s experience over the past decade suggests a more nuanced relationship. A closer look at previous election cycles shows that movements in inflation and NGX-ASI returns were often shaped less by election spending and more by broader macroeconomic developments such as exchange-rate adjustments, oil price shocks and policy shifts.

Understanding this relationship is important because inflation dynamics affect equity valuations through both discount rates and corporate earnings expectations. Asset prices reflect discounted expectations of future cash flows, and both the expected level of cash flows and the discount rate investors apply are sensitive to macroeconomic conditions. Rising inflation may increase nominal interest rates and compress valuation multiples. At the same time, firms may face margin pressure when input costs rise faster than selling prices.

However, the relationship between inflation and equity returns is not always stable. Academic research increasingly suggests that the impact of inflation on equities depends on the broader macroeconomic environment and the nature of the inflation shock. For instance, Cieslak and Pflueger (2023) argue that not all inflation episodes have the same implications for financial markets, noting that demand-driven inflation can have very different effects on asset prices compared to supply-driven inflation. Similarly, Bhamra et al. (2023) show within an asset-pricing framework that higher expected inflation can coincide with lower equity valuations due to nominal rigidities and valuation effects, even in situations where default risk declines.

Empirical evidence also points to strong state dependence in the inflation–equity relationship. Connolly et al. (2022) find that the relationship between stock returns and inflation shocks becomes economically significant mainly during periods of weaker economic conditions, with both the sign and magnitude of the relationship varying across different macroeconomic regimes. This suggests that the impact of inflation on equity markets cannot be assumed to be constant over time.

Beyond the level of inflation itself, the risk associated with inflation also plays an important role for asset prices. Boons et al. (2020) show that inflation risk is priced in stock returns and that inflation risk premia vary significantly over time, sometimes even changing sign across decades. In some cases, rising inflation signals weaker future economic activity and declining purchasing power; in others it reflects stronger demand conditions. For investors, this means that the uncertainty surrounding inflation can matter just as much as the inflation level itself.

Inflation Dynamics Around Election Cycles

A review of Nigeria’s recent election cycles reveals patterns that challenge the common perception that elections directly drive inflation.

In the run-up to the 2015 general election, headline inflation actually moderated slightly. Inflation declined to 8.0% in 2014 from 8.5% in 2013. Inflation later increased to an average of about 9.0% in 2015, with most of the increase occurring in the second half of the year.

In our view, the increase in prices in 2015 was not primarily driven by election spending. Instead, it reflected the currency depreciation that followed the sharp decline in global crude oil prices at the time. The inflationary impact of exchange-rate pressures became even more pronounced in 2016, when the Central Bank of Nigeria moved toward a more flexible exchange-rate regime.

During the 2019 election cycle, headline inflation actually moderated. Inflation declined from 18.7% in January 2017 to 11.4% by the end of 2018, and continued easing after the election, reaching a 44-month low of 11.02% in August 2019. Inflation began rising again later in 2019, largely due to the border closure policy introduced by the Buhari administration, which disrupted food supply chains and pushed food prices higher.

Inflation dynamics in the 2023 election cycle also followed a different pattern. While inflation increased during 2022 and 2023, much of the pressure was driven by food inflation rather than core inflation, suggesting supply-side factors rather than election spending. The largest inflation shock actually occurred after the election, driven by major policy reforms such as exchange-rate liberalization and the removal of fuel subsidies.

Taken together, these episodes suggest that inflation movements during election periods were often driven more by macroeconomic shocks and policy decisions than by election spending itself.

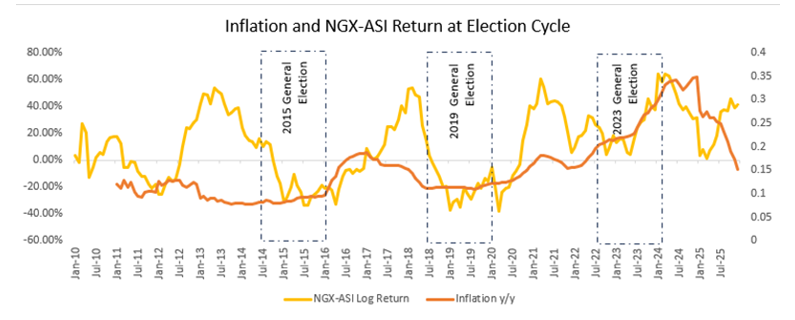

Source: NBS; Investing.com; Gifted Analysts

Figure above compares Nigeria’s headline inflation with NGX-ASI log returns across the last three election cycles. The chart shows that while election periods often coincide with higher market volatility, inflation itself does not follow a consistent pattern around elections. In the 2015 cycle, inflation pressures were largely driven by exchange-rate depreciation following the collapse in oil prices. In the 2019 cycle, inflation moderated before the election and only rose later due to the border closure policy. The 2023 cycle again demonstrates that the largest inflation shocks occurred after the election following major policy reforms. This evidence suggests that macroeconomic shocks and policy decisions, rather than election spending alone, have been the dominant drivers of inflation dynamics.

Equity Market Behaviour During Election Cycles

The behaviour of the Nigerian stock market during election periods has also varied across cycles.

During the 2015 election cycle, the NGX All-Share Index (ASI) experienced significant declines. In the pre-election year of 2014, the market closed the year with a return 17.6% loss, with the major sell-off beginning around October 2014. Several factors contributed to this downturn, including rising political uncertainty, falling oil prices, foreign-exchange scarcity and capital flight. Foreign portfolio investors reduced their exposure to Nigeria significantly during this period. In fact, foreign portfolio inflows in the second half of 2014 declined by 13.4% compared to the first half of the year. The decline continued into 2015, when the market recorded a 31.6% loss in January and eventually closed the year down 19%. Investor sentiment was further weakened by fears of election-related violence and the postponement of the elections, which increased investor apathy and triggered a significant sell-off. Indeed, foreign investors’ participation in the Nigerian stock market dropped significantly, from a peak of 61.4% contribution to equities market turnover in 2012 to 45.0% in 2016.

A similar pattern was observed in the 2019 election cycle. After a strong start to 2018, when the market recorded returns above 50% in January and February, the market began experiencing significant sell-offs in the second half of the year and eventually closed 2018 down –15.7%. The decline was driven by several factors, including political uncertainty, weaker-than-expected GDP growth and declining business confidence. According to the CBN’s Monthly Business Expectations Survey, business confidence began deteriorating around July 2018. Additionally, delays in the passage of the 2018 federal budget slowed economic activity and weakened market sentiment. By the 2019 election year, the market remained under pressure, with the ASI recording average negative returns of around 24.7% loss.

The 2023 Election Cycle presented a Different Outcome

The market delivered positive returns in both the pre-election year and the election year. In 2022, the NGX-ASI demonstrated notable resilience by ending the year with a gain of 18.2%, despite aggressive monetary tightening by the Central Bank of Nigeria. During that year, the CBN raised the Monetary Policy Rate four times, increasing it from 11.5% to 16.5% by November 2022.

Despite the tightening cycle, equities remained attractive for several reasons. Global oil prices surged following the Russia-Ukraine conflict, boosting the NGX Oil and Gas Index by about 48.06% and supporting the broader market. At the same time, strong corporate earnings provided a cushion for equities. In Q1 2022, major companies delivered weighted average earnings growth of about 36.3%, alongside dividend yields of around 5.2%, making equities attractive relative to fixed-income returns.

In 2023, the NGX-ASI delivered even stronger performance, recording an average monthly return of about 23.1%. The rally was largely driven by investor optimism around market-friendly reforms introduced by the new administration, including the removal of the long-standing fuel subsidy and the unification of the foreign-exchange market. These reforms improved investor sentiment and increased confidence in the long-term outlook of the Nigerian economy.

Sector Behaviour During Election Cycles

The below figure shows the log returns of major NGX sector indices over time. Our major observation is that most sectors tend to move in similar directions during election cycles. This suggests that election-related uncertainty often affects overall market sentiment rather than specific sectors in isolation.

However, when we move from sector indices to individual stocks, a clearer picture emerges.

Source: Investing.com; Gifted Analysts

The movement of the overall market during election cycles has often been significantly influenced by a few large-capitalization stocks, particularly Dangote Cement (DANGCEM) and GTCO. Because these companies carry substantial weights in the NGX-ASI, their price movements can have an outsized impact on the direction of the broader index.

For instance, during the 2014 pre-election year, Dangote Cement declined by 20.5%, contributing approximately 40.5% to the overall decline in the ASI. The drop was largely driven by company-specific factors, including a 20.5% fall in earnings per share and a 3.2% decline in profit before tax. GTCO (then GTBank) also contributed to the market decline during that period. The stock fell by 11.1% in 2014, accounting for roughly 7.2% of the ASI’s decline. This was partly linked to a 9.1% drop in profit after tax, alongside tighter banking regulations, including an increase in the Cash Reserve Ratio (CRR). Hence, two stocks (GTCO and DANGCEM) alone accounted for 47.9% of ASI’s decline in 2014.

A similar pattern appeared in 2018, when Dangote Cement declined by 17.5%, closely mirroring the broader market decline during the pre-election period.

These episodes suggest that declines observed during pre-election periods were often driven by idiosyncratic company-level developments rather than broad election-related fears.

What Should Investors Expect?

As Nigeria approaches another election cycle, markets are likely to price short-term political uncertainty, which may lead to temporary downside pressure on equity prices. However, historical evidence shows that election periods do not automatically translate into sustained market declines.

If inflation continues to moderate, foreign-exchange relatively stable, and policy reforms stay credible, the broader market environment should remain supportive for equities. That said, election periods often trigger sentiment-driven caution among investors. This can lead to short-term dips or profit-taking as investors temporarily reduce risk exposure while awaiting clearer political outcomes.

For investors, such pullbacks may present opportunities to accumulate fundamentally strong stocks rather than signals of a structural market downturn. Ultimately, while elections may influence sentiment in the short term, macroeconomic fundamentals and corporate earnings remain the primary drivers of long-term equity market performance.

Conclusion

Taken together, the evidence suggests that election cycles tend to amplify market volatility, but the underlying direction of the market is ultimately determined by macroeconomic conditions and corporate fundamentals rather than the election itself.